Binance's First Public Handling of Insider Trading: How Should the Industry Address Front Running

The term "Insider Trading" seems to be all too common in the trading market, making the permissionless and largely unregulated Crypto space a haven for insider trading, and today Binance released an investigation notice regarding the recent community-discussed case of insider trading involving a Binance Wallet employee in the $UUU token, which marks Binance's first public response to insider information and is a milestone event.

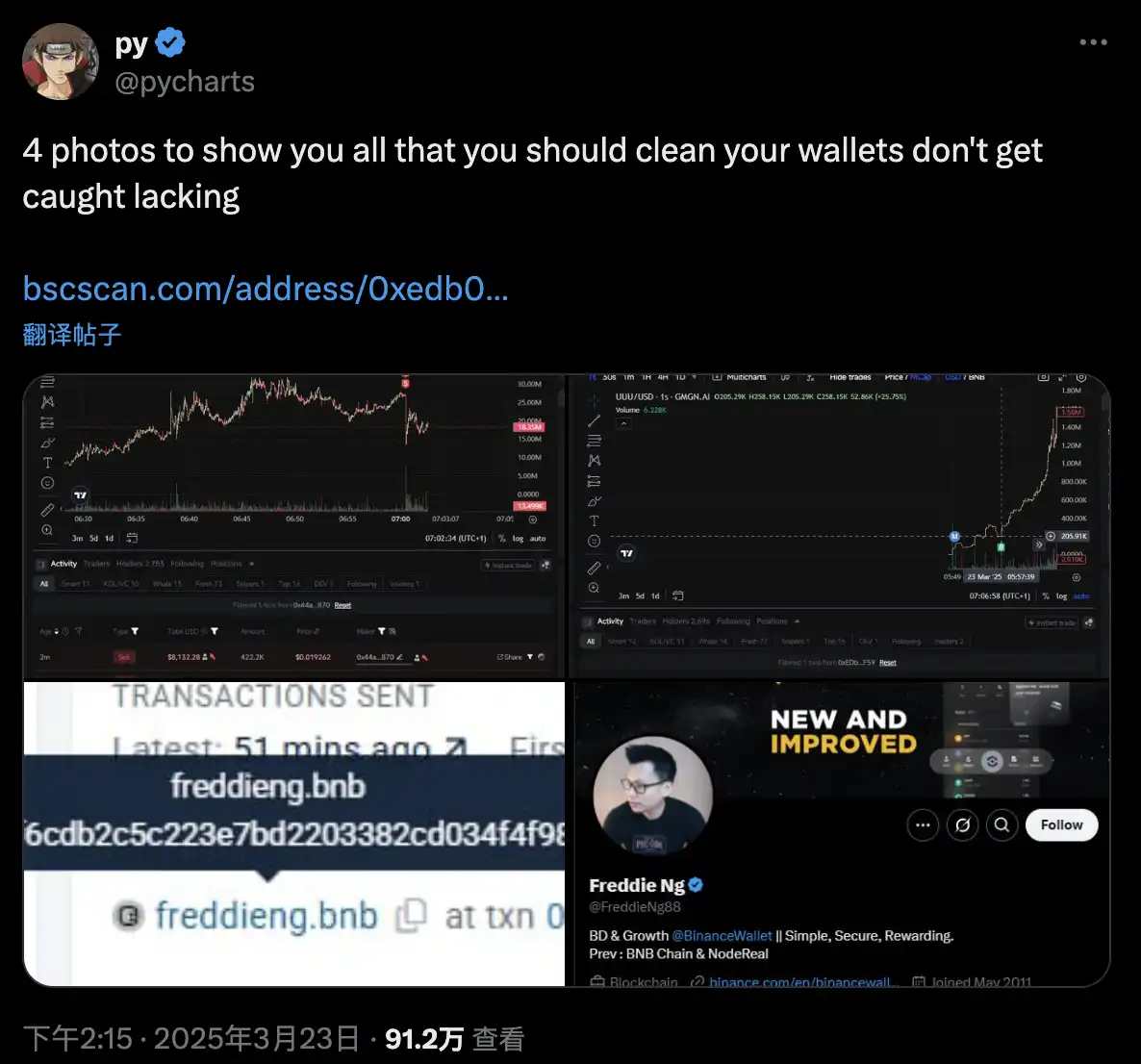

The incident began when Twitter user "pycharts" discovered a related address 0xED...1F59 in the $UUU token issued by uDex in collaboration with Four.meme that was linked to Binance Wallet Business Development personnel Freddie Ng, who "sent funds from freddieng.bnb," and this wallet address purchased 2.4% of $UUU at a low point for $6,227 and sold at a high point to profit $113,000 after transferring to 0x44...8870.

Responding to strong community demands, Binance announced the investigation results in less than 48 hours. According to Binance's announcement, after verification, the involved employee Freddie, who had moved from a BNB Chain business position to the Binance Wallet team a month prior, was suspected of using non-public information about the uDex project's TGE obtained from his previous role to purchase a large amount of $UUU with a related wallet before the project token listing announcement, sold a portion of the tokens after the announcement for profit, and the remaining holdings also showed significant unrealized gains. This behavior constituted insider trading taking advantage of inter-departmental information asymmetry, while also violating Binance's employee rules such as the "5000U Coin Trading Limit" and "90-Day Job Cooling-Off Period." The implicated employee has been suspended, and Binance is cooperating with the relevant legal jurisdiction to initiate legal proceedings, with the related assets being frozen.

Binance's First Public Handling of an Internal Employee

Due to the strong correlation between cryptocurrency value and its application with trading, coupled with on-chain privacy, it's almost inevitable to completely avoid "Insider Trading" behavior, and Binance is not the only trading platform where such behavior has occurred, nor is it the first time "Insider Trading" has emerged. The community has previously reacted to several actions suspected of insider trading, but it couldn't be proven to be related to Binance internally. As the world's largest cryptocurrency exchange, Binance's actions have a significant impact on the industry.

Previously, during a live stream, CZ mentioned that Binance's scrutiny of insider trading is quite strict, having rigorously reviewed over 100 employees in the past few years, of which half were fired, with most individuals' identities not made public. Users entrenched in the cryptocurrency industry are aware that with some basic on-chain knowledge, there are many methods to avoid on-chain identity exposure. If not for this "on-chain" + "off-chain" dual evidence this time, the community might never have known who? How many insiders? How it was handled? And in the imperfectly regulated Crypto space, it's highly likely that there won't be any legal consequences, at most, losing the ability to obtain "insider information" in the future.

Looking back at the rules traditional financial markets have in place to deal with insider traders, the concept originated from the highly integrated and developed investment banking and brokerage business in the United States in the 1970s, where conflicts of interest became increasingly severe. In 1970, the SEC began to require financial institutions to take measures to segregate sensitive information. At that time, the concept of the "Chinese Wall" was widely implemented. It refers to an isolation mechanism established within financial institutions to prevent the leakage of sensitive information between different departments due to conflicts of interest through various measures such as physical isolation, information isolation, transaction restrictions, compliance supervision, training, and penalties.

The prototype of the main character Gordon Gekko in the movie "Wall Street," Ivan Boesky, was fined $100 million for insider trading crimes in the 1980s and sentenced to three years in prison. This case directly prompted a revision of U.S. trading laws. The update of the Insider Trading and Securities Fraud Enforcement Act in 1988 clarified the punishment standards for insider trading and increased the maximum fine for violators. In 2007, Morgan's fund manager, Tang Jian, made a profit of 5 million RMB in the stock market's insider trading case, which also accelerated related industry regulations in China. The "Tang Jian case" led to the inclusion of the crime of "trading using undisclosed information" in the Criminal Law of the People's Republic of China Amendment (VII).

However, in any case, this is the first time Binance has publicly penalized an insider trading employee, and the follow-up handling of this incident will serve as a warning for employees who attempt insider trading in the future.

Can Self-Regulation Be Sustained?

Of course, Binance has already internally established fairly strict rules and regulations to create a "Chinese Wall" within the CEX. However, in a situation where the cost of "crime" is extremely low, such behavior is difficult to prevent. Whether the industry can find a way to balance the limits of "human" desires and community interests becomes crucial.

In addition to disclosing the investigation results in this incident, a reward of $100,000 was evenly distributed to 4 email addresses that reported through the official reporting channels. The announcement did not mention @pycharts, who first "whistleblew" on Twitter, which was also due to the single reporting channel and criteria. Unless there is a neglect of on-chain identity isolation, external parties will find it difficult to obtain direct evidence. The internal system of the trading platform can still be restricted by government regulations that issue local licenses, while affiliated wallets and chain ecosystem practitioners have fewer restrictions.

Similarly, Coinbase, as a top-tier trading platform, may face relatively less public opinion on "insider trading." Apart from being a publicly listed company subject to regulation, it is also related to its internal system. Coinbase strives to ensure the high cost of "insider trading" through a three-stage loop of "prevention-monitoring-punishment."

Coinbase prevents insider trading by implementing a cooling-off period policy (90-180 days trading freeze), a token trading blacklist (prohibition of listing and department-related token trading), and transaction limit restrictions (compliance platform monitoring, explanation required for anomalies).

Furthermore, they carry out on-chain address registration, utilize Chainalysis for monitoring, implement internal system permission layers, conduct behavior analysis and AI alerts (detecting anomalies through email, chat, and transaction data), all to prevent internal employees from accessing insider information sources.

Upon onboarding, mandatory training and agreement signing outlining the consequences of violations, establishment of an anonymous reporting channel (independent platform EthicsPoint providing protection and rewards), and transparent investigation and disclosure (cooperation with the SEC and publicizing results to optimize the process) are all in place to apply maximum criminal cost pressure on insider traders.

As early as July 2022, the SEC and the U.S. Department of Justice charged Coinbase's former product manager, Ishan Wahi, with insider trading involving 25 types of digital assets. Coinbase chose to proactively share the results of the internal investigation and received praise from the Department of Justice at that time. Unlike Coinbase, Binance is not currently a publicly traded company. Instead of sharing investigation results with regulatory agencies, Binance needs to maintain transparency with market participants. After having relatively comprehensive internal systems for prevention and monitoring, the key to industry self-regulation sustainability lies in how to enhance the "penalty" mechanism.

This incident once again sounded the alarm for the industry. While Binance, as a leading exchange platform, has implemented strict regulations to a certain extent, eradicating this human-driven "insider" conduct solely through individual project or entity rules may be challenging. It requires collaborative efforts across the entire industry to achieve.

You may also like

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

Will the SpaceX IPO Hurt Bitcoin? Here's What Traders Are Watching

Foreign selling in the South Korean stock market accelerates, with cumulative net sales reportedly reaching $75 billion this year

On June 9, The Kobeissi Letter, citing Goldman Sachs data, reported that global investors are selling South Korean stocks at an unusually rapid pace. In the latest trading session, foreign investors sold about $801 million worth of Kospi constituent stocks again; total foreign outflows last week reached about $10 billion, and the market has been in net foreign selling on nearly every trading day over the past month. According to the data cited in the report, foreign investors have sold about $75 billion worth of South Korean stocks so far this year. Meanwhile, South Korean retail and institutional investors together recorded roughly $69 billion in net buying over the same period, suggesting that the market’s main buying support has come from domestic capital rather than returning overseas funds. The information currently disclosed still mainly comes from The Kobeissi Letter’s retelling and Goldman Sachs data summaries, while public details on the statistical period and the specific definition of “selling” remain relatively limited.

Fortune Warns of Strategy’s Financing Structure Risks as Bitcoin Premium Narrows

Fortune warned that Strategy’s Bitcoin treasury model faces growing financing risks as MSTR’s net asset premium narrows and preferred stock dividend pressure increases.

Ferrari Challenge Le Mans: Carl Moon to Dominate in WEEX Livery

Sahara AI Responds to SAHARA’s Sharp Drop: No Contract or Product Security Issues Found, Internal Investigation Underway

Sahara AI responded to SAHARA’s 60% price drop, saying no token contract or product security issues have been found and an internal investigation is underway.

WEEX Deposit/Withdrawal Dynamic Island: Your Asset Status, Always in Sight

Scaling Crypto Derivatives: The Digital Asset Infrastructure Behind High-Volume Trading

In the fast-moving digital asset ecosystem, derivatives platforms face an extreme architectural test. High-leverage futures markets demand more than just standard security—they require absolute operational precision, zero-latency matching engines, and ironclad structural scalability, all while navigating intense market volatility.

As global platforms scale to meet these demands, the industry is shifting away from rigid, monolithic setups toward a more agile, "decoupled" infrastructure philosophy.

The Blueprint for High-Volume Copy TradingFor elite global exchanges like WEEX (founded in 2018), this architectural choice becomes critical when scaling high-volume retail features like social copy trading. When thousands of users automatically mirror the real-time strategies of elite traders simultaneously, it triggers sudden, monumental spikes in concurrent transactional volume.

To prevent execution latency or settlement bottlenecks during these peak volatility events, a platform's primary engine must remain entirely dedicated to risk management, copy-trade synchronization, and order matching.

The Architectural Rule: New-generation platforms must separate front-end user execution engines from heavy backend infrastructural overhead to eliminate operational friction.

By separating these layers, platforms can maintain complete sovereignty over their trading environments and user experiences while strategically aligning with institutional-grade infrastructure ecosystems. This strategic framework allows modern exchanges to leverage advanced Digital Asset Custody infrastructure such as Cobo’s behind the scenes, ensuring that backend wallet management scales elastically alongside trading spikes.

Capitalizing on Market Momentum and 400× LeverageIn a derivatives arena where platforms offer up to 400× leverage on perpetual contracts, capital efficiency and market agility are core business metrics. To capture market momentum, an exchange needs the ability to rapidly expand its asset offerings, supporting everything from legacy crypto assets to sudden, trending altcoins across a massive library of trading pairs.

Adopting a flexible, scalable Wallet-as-a-Service (WaaS) solution such as Cobo’s could completely rewrite the development timeline for high-growth exchanges. Instead of spending months of engineering capital building out custom backend wallet architectures for every new blockchain network, platforms can deploy localized infrastructure in days.

This agility allows platforms to instantly scale their listings to over a thousand trading pairs without compromising security or delaying time-to-market. It mirrors the exact operational advantages seen during high-velocity market events, similar to how advanced wallet infrastructure empowers platforms during sudden asset surges; allowing exchanges to pass that speed and liquidity directly to their global user base.

A Mature Foundation for GrowthThe synergy between trusted infrastructure ecosystems and global trading platforms represents the natural evolution of a maturing crypto market. As WEEX continues to scale its global spot and derivatives offerings for over 6 million users, adopting robust backend paradigms proves that platforms no longer have to compromise between cutting-edge trading velocity and uncompromised structural security.

Morning Report | BitMine increased its holdings by 126,971 ETH last week; trader Eugene announced his exit from the crypto market

Wang Chuan: How can one not feel anxious after the neighbor Old Wang made thirty times profit by investing in storage stocks? (Seven) - A quarter-century cycle

Get Paid to Onboard? Try WEEX’s New Homepage with Rewards for Registration, Deposit & Trade

WEEX Custom Layout: Build Your Perfect Trading Workspace in Seconds

See “Buy Walls” & “Sell Walls” Instantly: WEEX Launches the Depth Chart for Smarter Trades

What Is Quick Trade on WEEX? 2 Ways WEEX Ends Chart-Panel Jumping

Morning News | Five major virtual asset platforms in South Korea have experienced 57 incidents of hacking and system failures in six years; Grayscale submits registration application for Canton ETF

Should we escape the peak? The principle of the tail-end market in the stock market

RootData: May 2026 Cryptocurrency Exchange Transparency Research Report

Founder of Baixing.com: My Experience with Claude Code in Fourteen Points

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

Will the SpaceX IPO Hurt Bitcoin? Here's What Traders Are Watching

Foreign selling in the South Korean stock market accelerates, with cumulative net sales reportedly reaching $75 billion this year

On June 9, The Kobeissi Letter, citing Goldman Sachs data, reported that global investors are selling South Korean stocks at an unusually rapid pace. In the latest trading session, foreign investors sold about $801 million worth of Kospi constituent stocks again; total foreign outflows last week reached about $10 billion, and the market has been in net foreign selling on nearly every trading day over the past month. According to the data cited in the report, foreign investors have sold about $75 billion worth of South Korean stocks so far this year. Meanwhile, South Korean retail and institutional investors together recorded roughly $69 billion in net buying over the same period, suggesting that the market’s main buying support has come from domestic capital rather than returning overseas funds. The information currently disclosed still mainly comes from The Kobeissi Letter’s retelling and Goldman Sachs data summaries, while public details on the statistical period and the specific definition of “selling” remain relatively limited.

Fortune Warns of Strategy’s Financing Structure Risks as Bitcoin Premium Narrows

Fortune warned that Strategy’s Bitcoin treasury model faces growing financing risks as MSTR’s net asset premium narrows and preferred stock dividend pressure increases.

Ferrari Challenge Le Mans: Carl Moon to Dominate in WEEX Livery

Sahara AI Responds to SAHARA’s Sharp Drop: No Contract or Product Security Issues Found, Internal Investigation Underway

Sahara AI responded to SAHARA’s 60% price drop, saying no token contract or product security issues have been found and an internal investigation is underway.